Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

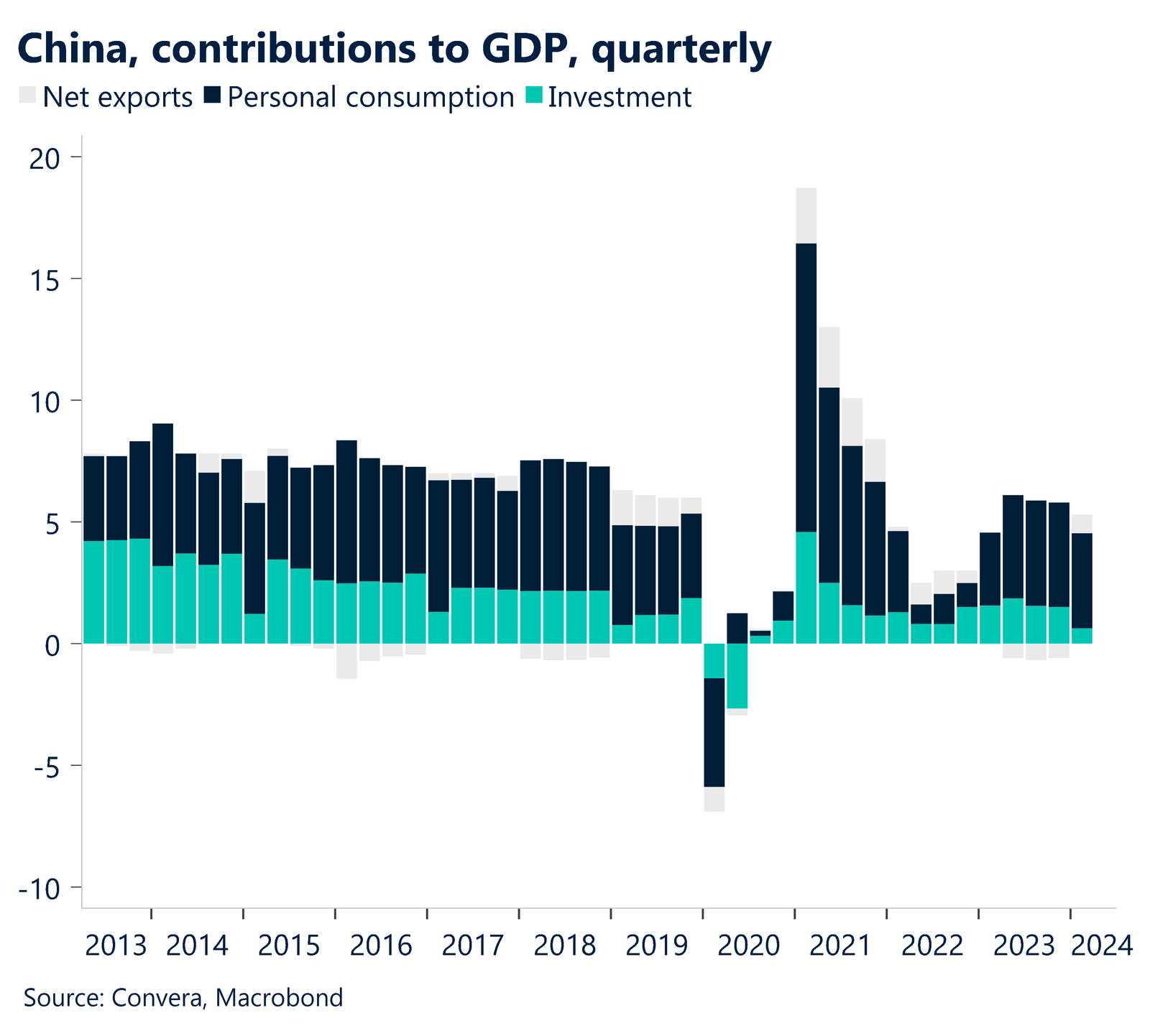

China slowdown hits regional FX

The Australian dollar and other APAC currencies fell yesterday after a sequence of weaker Chinese data caused regional markets to worry about China’s potential drag on economic growth.

Most notably, second-quarter GDP came in at 4.7% in annual terms – down from 5.3% last quarter and below forecasts for 5.1%. June retail sales were also sharply below forecasts although industrial production was better than expected.

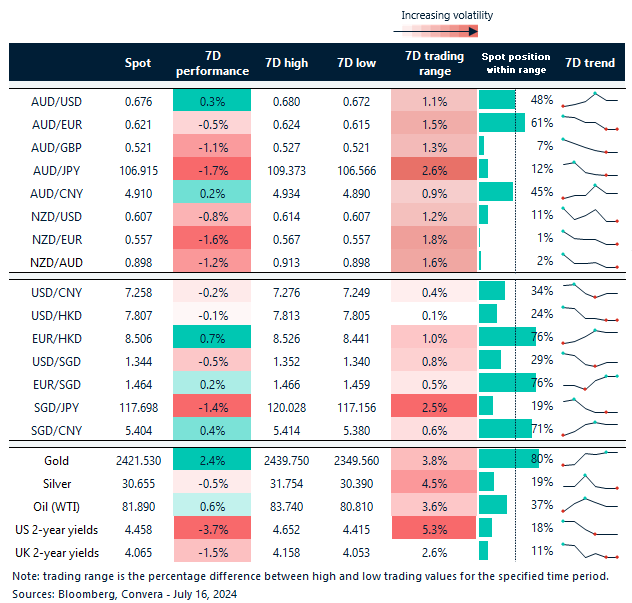

The AUD/USD ended the session down 0.4%.

The NZD/USD was even weaker – falling 0.8% – not helped by a big drop in the BusinessNZ services index.

The USD/CNH gained 0.1% while USD/SGD climbed 0.2%. USD/JPY gained 0.2%.

In other markets, GBP/USD fell 0.2% while the euro outperformed, down only 0.1%.

USD index rebounds from three-month lows

The US dollar was well supported overnight, gaining moderately, despite further commentary from Federal Reserve chair Jerome Powell that suggested the Fed was more confident inflation was returning to its 2.0% target after last week’s June CPI report saw price pressure ease quicker than expected.

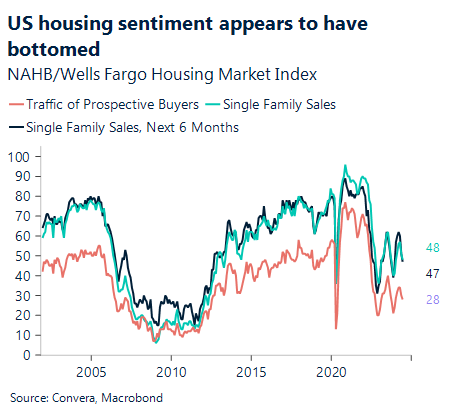

Looking to the US housing market, sentiment has recently declined. In July, we anticipate that the NAHB house builders’ confidence index, due Tuesday night, will stay at 43. Since April, sentiment has been deteriorating, and in recent months, home builders have shown a heightened sensitivity to mortgage rates.

Both mortgage rates and mortgage applications for purchases have been comparatively steady since June. We don’t anticipate a big shift in house builders’ mood in July given the lack of a discernible improvement in housing circumstances.

While the greenback, as measured by the USD index, has fallen to three-month lows, the US dollar’s now at key support and any decline might be brief and not be sustained in the medium run.

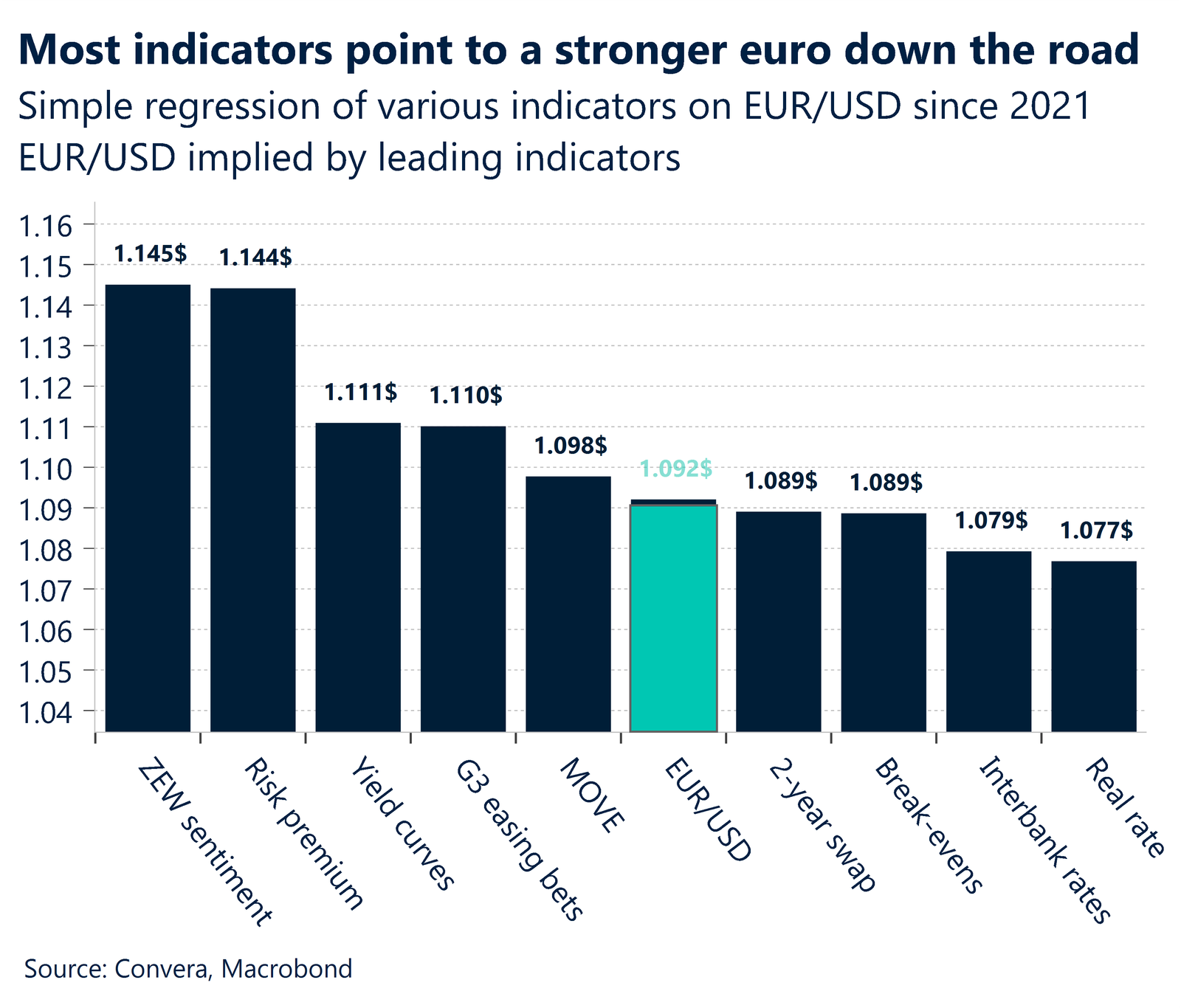

Euro gains on ECB policy shift

The euro’s recently been stronger with the EUR/USD at four-month highs and EUR/SGD nearing eight-month highs. The AUD/EUR has recently eased from one-year highs.

The Q1 2024 ECB Bank Lending Survey, credit requirements for business loans became more stringent; nevertheless, this tightening was slower than in the Q4 2023 survey.

On the other hand, loan requirements for homes relaxed. Banks had predicted a comeback, but in Q1 2024, business loan demand declined more sharply than in Q4 2023, while housing loan demand slightly decreased overall.

Overall, the latest Bank Lending Survey suggests that the ECB’s aggressive tightening program appears to be slowing down.

With the Q2 report due tonight, we anticipate that the Bank Lending Survey will soon start indicating an improving financial economy, given that the ECB has now reduced rates in June and is anticipated to do so gradually going forward. Demand should increase in comparison to previous reductions, and lending conditions should start to improve, laying the groundwork for further improvement in the European economy.

Aussie turns at highs

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 15 – 19 July

All times AEST

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}