A weaker yen is a boon for Japanese exporters’ profits, and for tourists visiting Japan who find their currencies going further, but it squeezes households by increasing import costs.

Here are some of the reasons for the slide:

Rates

Interest rates and momentum are powerful forces in foreign exchange markets. Both are against the yen. The Bank of Japan left short-term Japanese interest rates between 0 and 0.1 per cent in April and did not indicate sharp or sustained rises were coming up ahead.

These deals, known as a “carry trades” are particularly attractive when broader market volatility is relatively low, as it is right now, as the fundamental rate difference can drive the markets.

Short-term US rates are at 5.25-5.5 per cent, and a US rate cut isn’t expected until November or December.

02:42

Japanese monetary authorities mull intervention options after yen drops to 34-year low

Japanese monetary authorities mull intervention options after yen drops to 34-year low

Momentum

Why is the yen falling? Because people are selling it. And why are people selling? Because it is falling. Such can be the self-fulfilling loop of the market mindset.

The yen has been steadily sliding for more than three years and has lost more than one-third of its value since the start of 2021 and few are game to stand in the way.

The trend discourages exporters from converting foreign proceeds into yen. It encourages Japanese financial institutions to invest abroad. And it has been a boon for speculators betting against the yen, who have not been shy.

Speculators’ short-yen positions hit their largest since 2007 in the week ended April 23.

Outlook

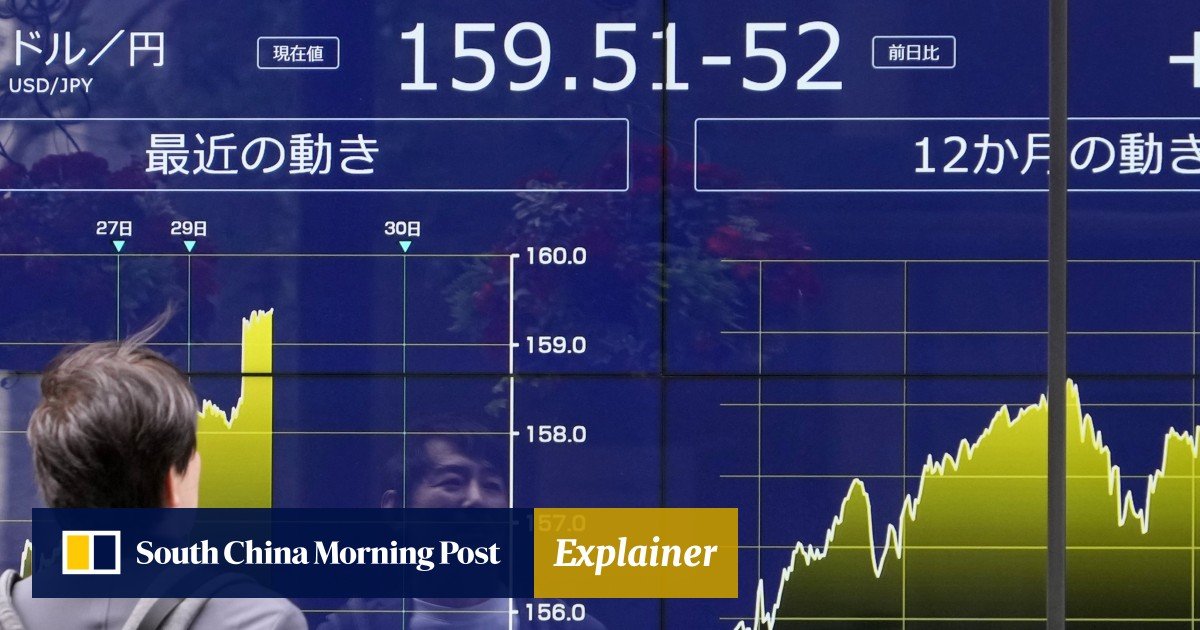

The BOJ’s decision to leave policy unchanged at its April meeting and to offer no fresh hints of hikes seemed to unleash a new wave of yen selling that drove the currency, briefly, weaker than 160 per dollar for the first time since 1990.

The rates picture is also keeping big Japanese investors’ cash abroad, where it can earn better returns.

Japan Post Bank and Japan Post Insurance, among the largest financial firms, told Reuters their portfolios won’t be radically changing in response to the BOJ’s March shift.

07:43

From economic ‘miracle’ to cautionary tale: Japan’s development and recession

From economic ‘miracle’ to cautionary tale: Japan’s development and recession

Response

The yen rose sharply over a few hours in the Asia daytime on April 29, leading traders to suspect that after weeks of threatening to intervene, Japan had stepped in to support its currency.

Japan’s top currency diplomat Masato Kanda declined to comment when asked if authorities in Tokyo had intervened. In any case, the risk of intervention at these levels is high enough that few wanted to stand in the way of the yen’s rebound.

Real terms

A real effective exchange rate index value of 70.25 for the yen in February is the lowest since the Bank of International Settlements’ records began in 1994 and lower than any of the Bank of Japan’s retrospective projections, which date to 1970.

That means tourist dollars go further than they have for generations, and that has the tourism industry booming. Japan’s current account has been in surplus for 13 months with help from tourism income, and February’s 2.79 million visitors was a record for the month.

Domestic consumption, however, has been a weak spot in Japan’s fragile economic recovery as households tend to be net importers and face higher prices due to a weak yen.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}