Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

Oil surge supports Aussie

The Australian dollar traded at three-week highs overnight as worries about renewed tensions in the Middle East saw oil prices surge higher on Monday.

WTI crude jumped 3.2% as it moved back above USD80 per barrel for the first time in a month as the US warned of potential attacks by Iran in the Middle East – potentially as soon as this week.

The rise in energy prices supported the commodity currencies. The AUD/USD gained 0.2% ahead of a key wage price index number due at 11.30am AEST.

The NZD/USD gained 0.4% while USD/CAD bucked the trend with a 0.1% gain.

US shares were mostly weaker on these geopolitical tensions with the Dow Jones down 0.4% while S&P500 was flat. The Nasdaq gained 0.2%.

In Asia, the US dollar was mostly higher, with USD/JPY up 0.4%, USD/CNH up 0.1% and USD/SGD flat.

EUR resilience waning?

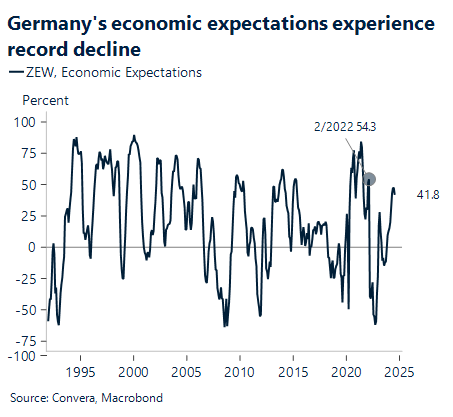

In Europe, the euro has been remarkably resilient over the last month, outperforming all G10 currencies apart from the safe haven Japanese yen and Swiss franc.

That said, a recent reversal in the EUR/USD at the year-to-date highs at 1.1000 suggests the risk of a move lower.

In keeping with the August Sentix poll, we anticipate a significant decline in the German ZEW for August.

This decline is mostly the consequence of the continued sell-off in global risk due to worries that central banks have maintained policy rates too high for too long.

Any move lower in EUR/USD would initially target the 1.079-1.083 cluster of short-term support levels.

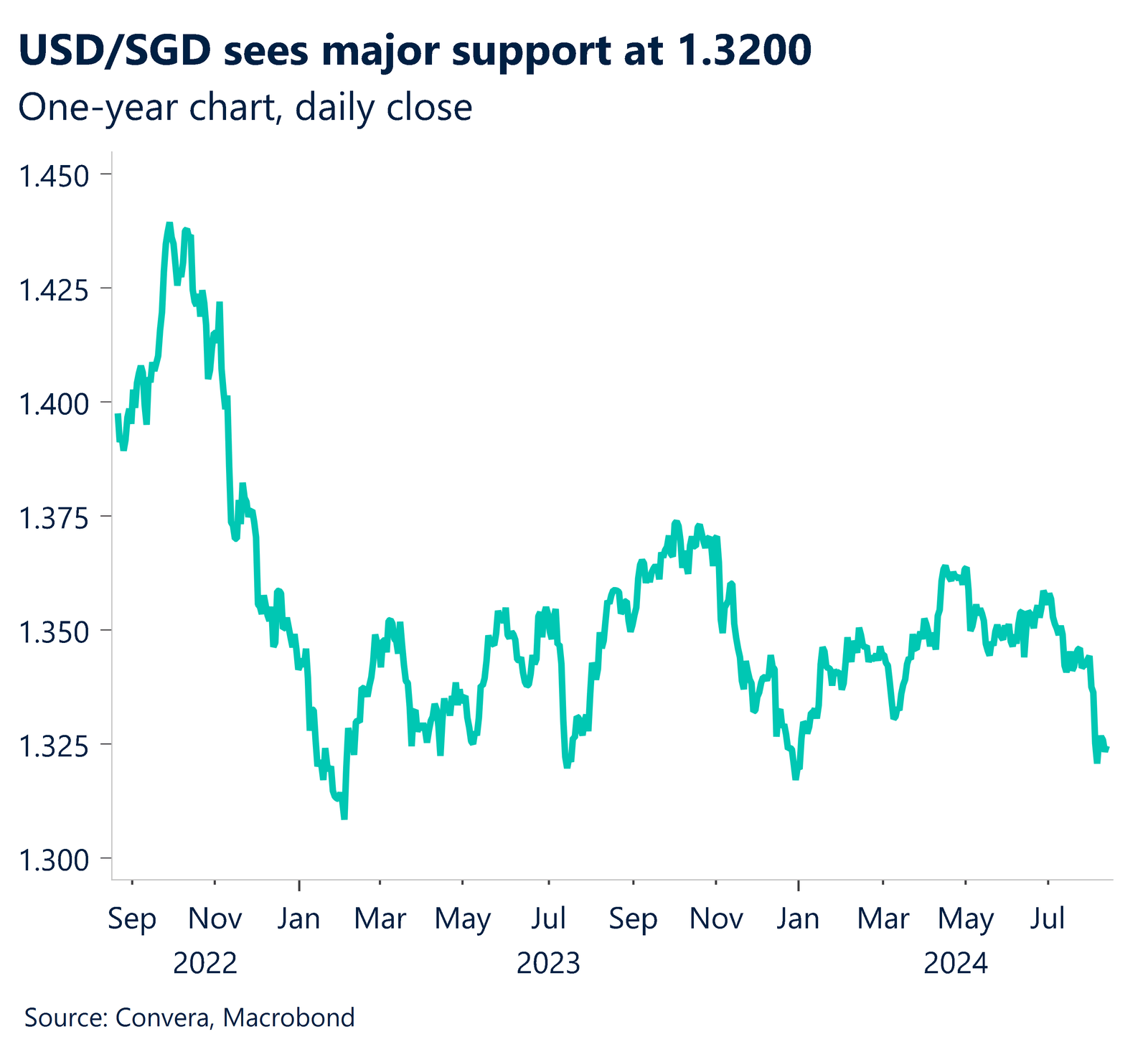

SGD mildly negative, support seen at 1.3200

Singapore June-quarter GDP is due at 8.00am SGT (10.00am AEST). Because of the unexpected decline in industrial output in June, we anticipate that the final estimate of Q2 GDP growth will be revised down from the advance estimate of 2.9% to 2.6% y-o-y.

Even with the revised negative estimate for the final Q2 GDP, given our estimate of 2.8% GDP growth in H1, we still anticipate the Ministry of Trade and Industry (MTI) to increase its full-year prediction range to 2.0-3.0% from 1.0-3.0%.

The Monetary Authority of Singapore (MAS), which stated last month that it anticipated GDP growth to occur in the top half of the MTI’s projection range, concurs with our assessment.

In accordance with market expectations, MAS maintained the S$NEER slope, band, and mid point in its July Policy Meeting Statement. MAS’s assessment of inflation does have some dovish aspects, though: 1) a slight lowering of the headline inflation projection, and 2) an admission of slower QoQ core inflation.

As such, with a mildly negative view on the SGD, this sets up the USD/SGD to rebound from the major support zone seen at 1.3200.

Aussie at highs as oil jumps

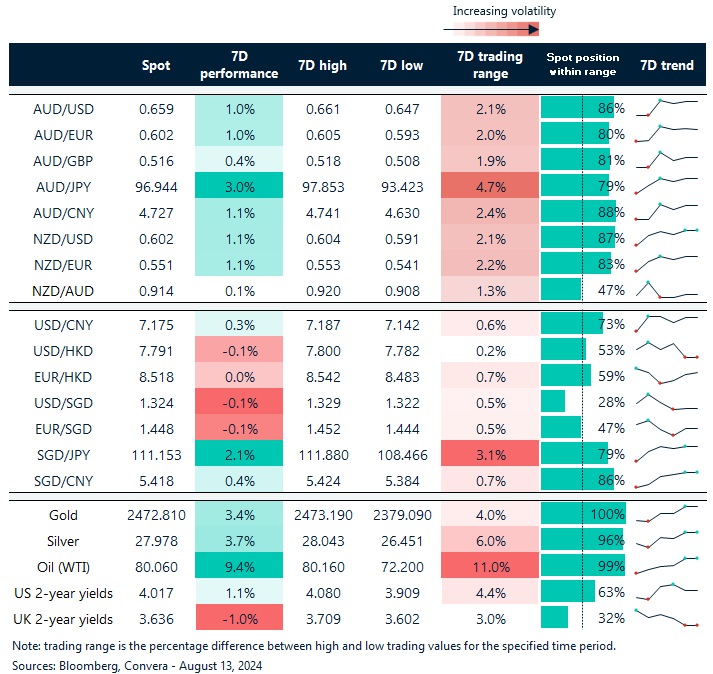

Table: seven-day rolling currency trends and trading ranges

Key global risk events

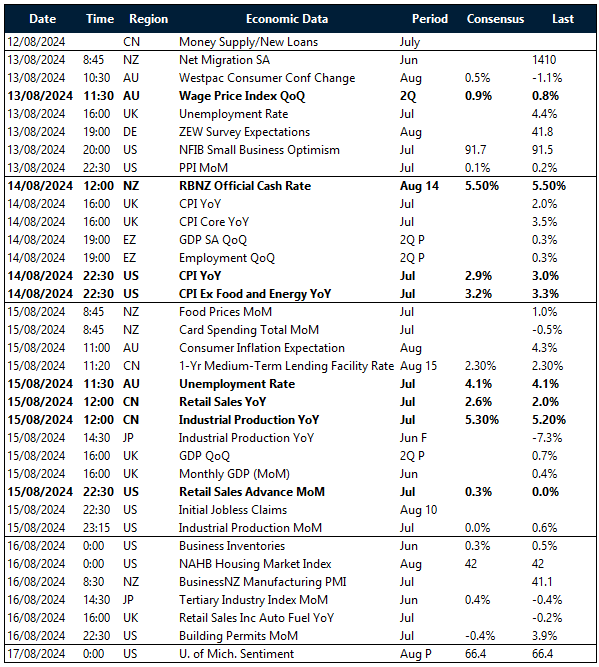

Calendar: 12 – 17 August

All times AEST

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}