Yuji Sakai

The U.S. Dollar Index (DXY) has recently pulled back as the currency faces the start of Fed rate cuts, but the greenback’s losses may be curbed if the U.S. stock market can drive solid returns, Goldman Sachs said.

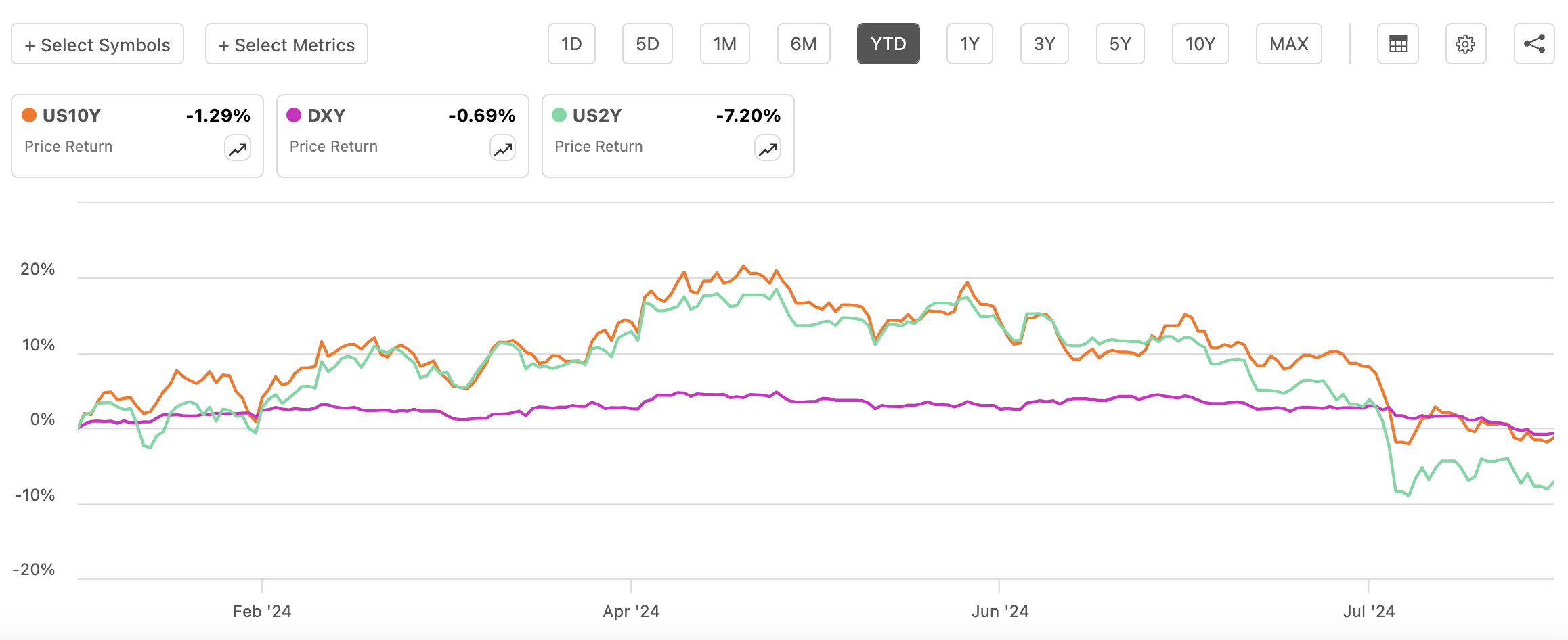

The Dollar Index (DXY) fell 1.7% last week, with losses against the Japanese yen (USD:JPY) contributing to the index’s worst weekly performance since November. The index slumped as the Federal Reserve affirmed expectations that rate cuts will begin this year. The (DXY) had been traveling down with Treasury yields (US2Y)(US10Y) as the prospect of rate cuts dims the relative attractiveness of those bond yields, pressuring dollar demand.

There are “justifiable reasons” to pare back long-dollar positions, Goldman said in Sunday note. “Global equity strength, along with improving global growth expectations and positive risk sentiment, are usually Dollar-negative,” and a key reason investors have chased soft-landing/weaker Dollar trades, Isabella Rosenberg on Goldman Sachs’ macro research desk said.

“However, we would caution that when U.S. equities are driving most of that global equity outperformance, the Dollar actually tends to strengthen,” Rosenberg said. Goldman said it has found the dollar this year has been as sensitive to equities as it has been to rates.

The S&P 500 (SP500) is among the top-performing stock indexes this year, rising by ~18%, including a near-return to its all-time closing high of 5,667 after a selloff this month. The MSCI World Index is also higher, but its gain is at ~15%. Germany’s DAX (DAX:IND) has risen ~11%, and Japan’s Nikkei (NKY:IND) has picked up ~14% in 2024.

The Dollar Index (DXY) has slipped ~0.5% YTD, with weakness coming in part from a recovery in risk sentiment. But “[if] the US economy and asset markets continue to deliver strong relative equity returns and a high risk-free rate to hedge portfolio risk, it will be challenging for the Dollar to decline in a material way,” Rosenberg said.

The November U.S. election is a key factor facing the dollar’s direction, but uncertainty about trade policy and fiscal spending “may still prevent meaningful outflows from the Dollar,” Rosenberg said. “Altogether, these factors mean that the Dollar’s rich valuation will not erode quickly or easily.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}