Whatever you think about Japan’s stock market, the past week has proved one thing: it’s not for the faint of heart. When the turmoil hit the markets, stock prices everywhere started to get hot under the collar. But none sweated harder than Japan.

Now, I’ve been investing in the land of the rising sun for a long time, and I know this move will have some folks rubbing their palms together and hunting for bargains. If you’re one of them, here are five things to consider.

What happened?

The value of stocks that changed hands in Japan’s main stock index, the Topix, hit a record on Monday with more than 8 trillion yen ($55 billion) on the move. Unfortunately, there was no Olympic gold medal to be won for the index: it lost more than 12%, its biggest single-day slide since 1987. (Over three days, it lost a total of 20%.) It’s managed to bounce back a little since then, but it’s still down more than 10% compared to last week and more than 16% from the highs reached just last month.

And that suggests this moment in Japanese stocks is one of two things: a bright-red warning signal or an opportunity. Here are six factors that can help you figure out which it is.

1. Japan’s corporate governance

The Japanese government has been encouraging companies to improve their focus on shareholders for the better part of a decade – and that’s changed the scene. A massive jump in the number and size of share buybacks in Japan, and an increased focus on investor returns and profitability have helped investors warm up to Japanese stocks.

2. Stock valuations

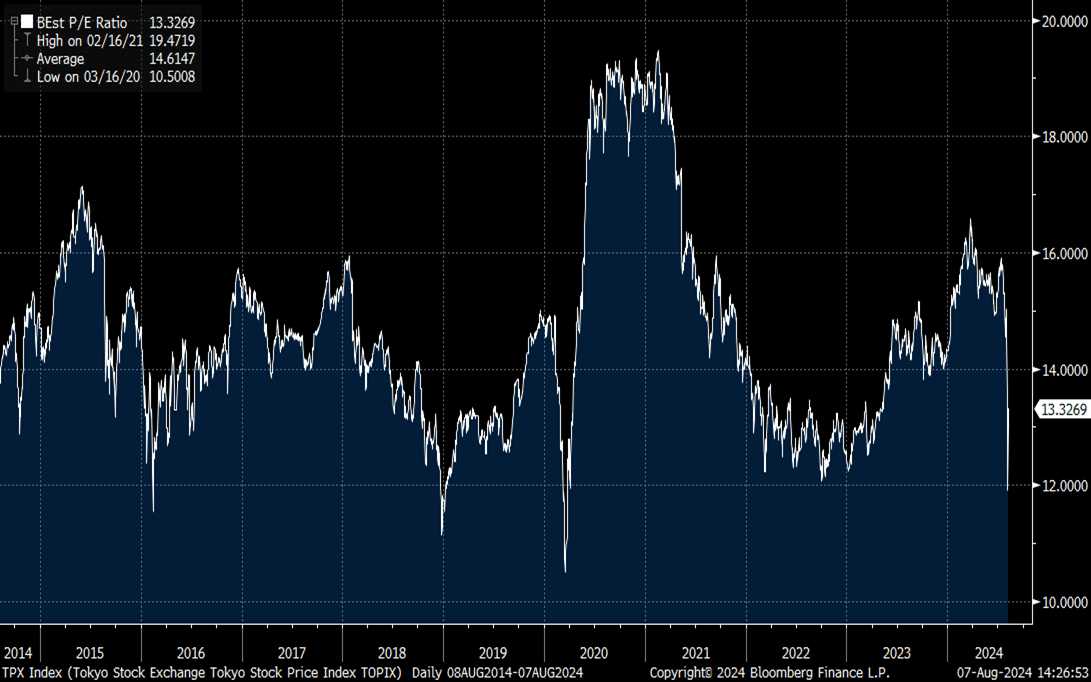

Stock valuations are an investor’s bread and butter, since they help determine long-term returns. And after this week’s sell-off, Japan’s key index – the Topix – is trading at an estimated forward price-to-earnings (P/E) ratio of 13x. That seems like a reasonably good deal, especially compared to the 16x it was going for just last month.

The Topix index’s estimated 12-month forward price-to-earnings (P/E) ratio from 2014 to 2024. Source: Bloomberg.

Problem is, that forward-looking figure might not be completely accurate, because the macroeconomic landscape can swiftly change. The “price” part of the index’s P/E ratio is certain: you just need to look at where the Topix is trading. The “earnings” part of the equation, on the other hand, is estimated. See, Japan sells loads of goods in the US and abroad, making its companies sensitive to changes in foreign exchange rates, especially the US dollar and the Japanese yen.

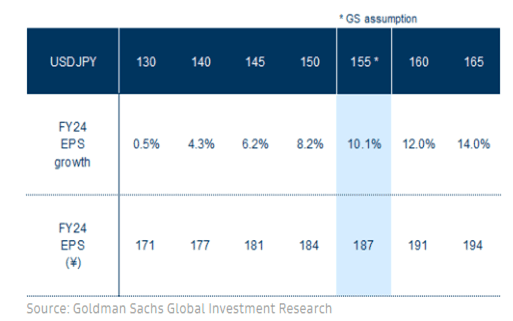

The Topix index’s estimated earnings per share, actual (bottom row) in Japanese yen, and growth (top row) in percentages for the next 12 months for the fiscal year ending March 2025 – depending on the value of the US dollar compared to the yen. Source: Goldman Sachs.

3. The yen.

The Japanese yen has been outmuscling all its rivals in the past week, as investors back out of the popular “carry trade”. This all happens in the currency, or forex, market, where trades happen in pairs, buying one country’s currency and selling another’s. A carry trade involves buying higher-yielding currencies – that is, ones from countries with higher interest rates – using funds borrowed in lower-yielding ones. And the yen’s been great for this for a long time, thanks to Japan’s very slim interest rates. Right now, thanks to the USD/JPY exchange rate, the US dollar buys about 155 yen – and at that rate, the estimated earnings per share (EPS) for the Topix index according to Goldman Sachs is around 187 yen. Now, to calculate the P/E ratio, you’d take the price of the Topix index 2,461 and divide it by the estimated EPS, 187 yen, which gives you a P/E ratio of 13.2x.

But things can change. During all the markets hullaballoo on Monday, the greenback was trading for just 142 yen – which would imply a Topix EPS of 179 and a P/E ratio of 13.7x. And that’s not quite as cheap.

And, look, the yen’s value against the US dollar has a massive impact on its stocks. Take a look at the Next Funds Topix ETF (ticker: 1306; expense ratio: 0.39%) and the USD/JPY trading pair. They often move to the same beat.

The US dollar versus the Japanese yen (blue line) and the Next Topix ETF (purple line), from 2014 to 2024. Source: Koyfin.

That’s one reason why the greenback’s sharp move from 160 yen to 145 over the past month has been accompanied by a nearly 20% drop in Japan’s stock market. And sure, the sell-off in stocks looks overdone if you’re just considering the move in the yen, but when too many sellers rush for the exits at the same time, markets can go into freefall.

4. Interest rates

The slowdown in the US economy and job market is expected to lead the Federal Reserve to lower its interest rates, with the first trim expected in September. These cuts will slim the gap between Japanese rates and US ones and make a big difference to both country’s currencies. After all, higher interest rates have made the US dollar more attractive to international investors and savers.

But that’s not the only thing that can narrow this gap: the Bank of Japan’s surprising interest rate increase last week also did a bit of heavy lifting. The move came as the country’s policymakers have become increasingly jittery about the weakening yen: its value has dropped 40% since 2022 and authorities’ efforts to buy up yen (selling boatloads of greenbacks in the process) had little impact. The rate hike successfully halted the currency’s decline, but it also led to a surprisingly hefty gain in the yen, which helped spark a 20% fall in Japan’s stock market. That, for sure, was not on their list of desired results.

And here’s proof of that: after the market moves, the BoJ said it would rule out further increases to interest rates while markets are “unstable”. That led the yen to weaken and Japanese stocks to rebound a little.

The whole thing had me thinking about the one radical policy device the BoJ used to have at its disposal: the ability to buy stock exchange-traded funds to support the the market when it falls. The Bank might be wishing they didn’t throw away that tool earlier this year: it might have helped stem (or maybe even prevent) this decline.

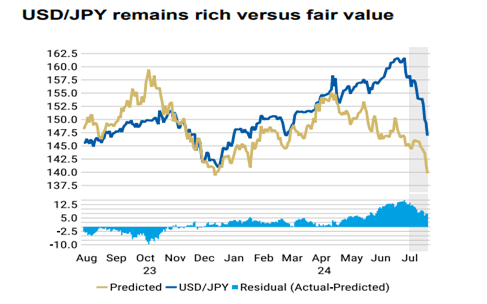

Morgan Stanley sees the US dollar as fairly valued at 137 yen. And sure, it’s notoriously difficult to predict currency moves, but the firm estimates that the gap between fair value and spot has dropped 60% after the recent shakeup.

Morgan Stanley’s estimates of fair value for USD/JPY and its recent trading, along with the percentage gap between the two. Source: Morgan Stanley.

Goldman Sachs has similar-looking targets for the trading pair, forecasting that the greenback will change hands for 130 yen in 2025, 125 yen in 2026, and 120 yen in 2027. If the investment bank’s correct, a move higher in the yen will likely weigh on Japan’s stocks – just as we have seen in recent days.

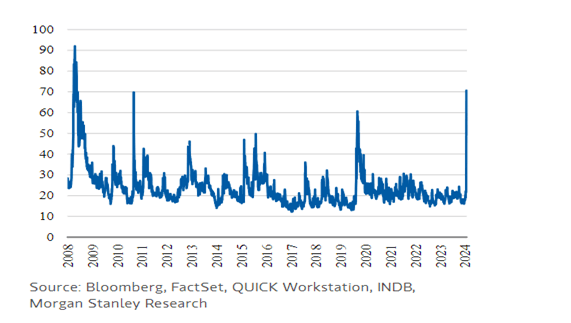

Japan’s volatility (a.k.a. fear) index jumped to 70 on Monday, for its highest level since 2008. The good news is that the index has since fallen back down to just 45. So if the traders who play in volatility-linked options are correct, the market is past the worst. But, make no mistake, 45 isn’t a small number, so there could be more big moves ahead.

The Nikkei 225’s Volatility Index, 2008 to 2024. Source: Morgan Stanley.

What’s the opportunity here?

After recent market turmoil, watching from the sidelines (or the beach) could be the smart move, and wait to see how it pans out. One key problem is that Japanese exporters, companies that are more sensitive to movements in the yen, have chunky weightings in both the Topix and the Nikkei 225 indexes, and their related ETFs. So when the yen increases in value, it usually pulls down their profits and share prices. So investing in domestic stocks – the ones that sell mostly in Japan – might be a better option now. That said, it’s hard to find an ETF that meets those exact criteria.

The iShares MSCI Japan Small-Cap ETF (SCJ; 0.5%) may be the most suitable pick out there, as small-cap stocks tend to have a more at-home focus and less international exposure. If you’re happy to ignore some of the risks and can buy individual stocks, you could simply follow Warren Buffett’s lead and buy some Japanese trading companies – his Berkshire Hathaway conglomerate owns around 8% of each of the big ones: Mitsubishi, Itochu, Marubeni, Mitsui, and Sumitomo Corp. Those behemoths all have fallen between 15% and 25% in the past month. Or, if you’re feeling a bit spendier, you could consider paying higher fees for an active fund that invests solely in the country’s domestic stocks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}