Japanese Yen continues to stand out as the strongest currency, in another day with a lackluster economic calendar. However, it’s Dollar that’s capturing market interest as markets enter into US session, where it has shown notable gains against major counterparts like Euro and Swiss Franc. Break of near term levels in both EUR/USD and USD/CHF suggests that the greenback’s near term rebound might extend further.

A key question now is whether the “Trump Trade” has returned, in particular particularly after Kamala Harris has solidified her position as the Democratic presidential nominee by securing necessary party and public support. The prospect of Donald Trump returning to the presidency and implementing his characteristic trade and tax policies could lead to stronger economic growth and higher inflation. These factors are expected to moderate Fed’s easing cycle, thereby supporting a stronger Dollar.

In the broader currency spectrum, Dollar’s momentum places it just behind Yen in terms of strength, followed by Canadian Dollar. At the other end, Australian Dollar languishes as the weakest, closely followed by New Zealand Dollar and then Euro. British Pound and Swiss Franc are positioned in the middle.

Technically, AUD/JPY’s fall from 109.36 resumed this week and accelerates to as low as 103.21 so far. Current development suggests that it’s now correcting whole rise from 86.04. Near term outlook will stay bearish as long as 105.76 resistance holds. Deeper fall should be seen to 38.2% retracement of 86.04 to 109.36 at 100.45. But strong support should be seen above 99.32 resistance turned support to bring rebound.

In Europe, at the time of writing, FTSE is down -0.28%. DAX is up 0.84%. CAC is down -0.17%. UK 10-year yield is down -0.0221 at 4.142. Germany 10-year yield is down -0.049 at 2.449. Earlier in Asia, Nikkei fell -0.01%. Hong Kong HSI fell -0.94%. China Shanghai SSE fell -1.65%. Singapore Strait Times rose 0.70%. Japan 10-year JGB yield rose 0.0181 to 1.063.

ECB’s de Guindos: Sep economic projections key for policy reassessment

In an interview with Spanish news agency Europa Press, ECB Vice President Luis de Guindos emphasized the significance of new macroeconomic projections in September, together with another two months of data on inflation and underlying inflation. These projections and data will help ECB reassess its monetary policy stance more effectively.

De Guindos stressed the importance of having more confidence that inflation will reach ECB’s target of 2% by the end of 2025, calling it the “key question.” He acknowledged the high level of uncertainty, stating that ECB must be “prudent” when making decisions.

He predicted that inflation will remain “around current levels until the end of the year” and observed that all measures of underlying inflation are declining. He added, “The disinflation process will continue from the start of next year.”

De Guindos also pointed out that wages are “starting to slow down,” and firms expect wage increases to moderate, particularly from 2025 onward. This moderation in wage increases is expected to lead to a reduction in services inflation, helping ECB achieve its 2% inflation target by the end of next year.

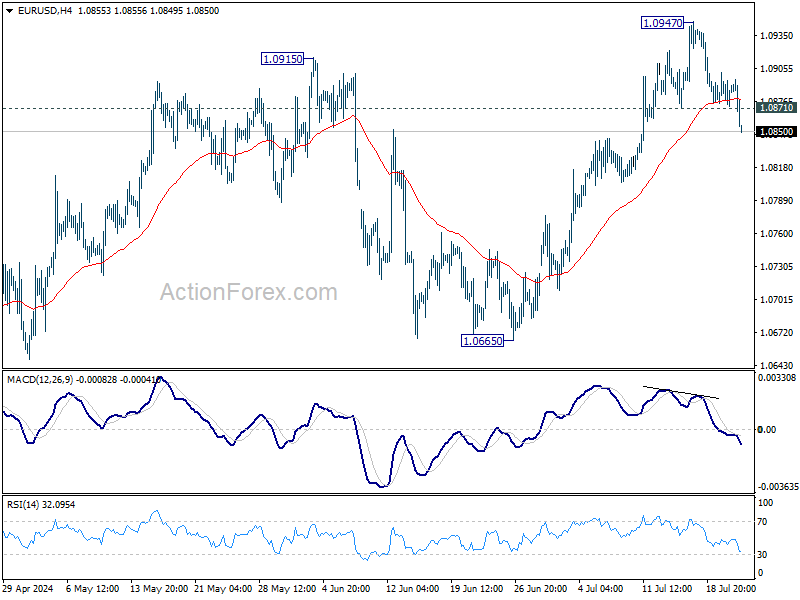

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0875; (P) 1.0889; (R1) 1.0905; More…..

EUR/USD’s break of 1.0871 support suggests that a short term top was already formed at 1.0947, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for 55 D EMA (now at 1.0810). Sustained break there will argue that whole rebound from 1.0601 has completed with three waves up to 1.0947, and target 1.0601/0665 support zone. For now, risk will stay on the downside as long as 1.0947 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that’s still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 14:00 | USD | Existing Home Sales Jun | 4.00M | 4.11M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jul P | -13 | -14 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}