Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

Chinese stimulus moves disappoint

The Australian dollar – and other key APAC currencies – opened lower on Monday after China’s highly anticipated stimulus briefing over the weekend disappointed markets.

After a massive rally in Chinese markets following a series of rate cuts and stimulus moves in late September, markets were looking for more detail from Saturday’s Finance Ministry briefing. The briefing provided further confirmation the government would support the property market and extend borrowing but lacked detail investors wanted.

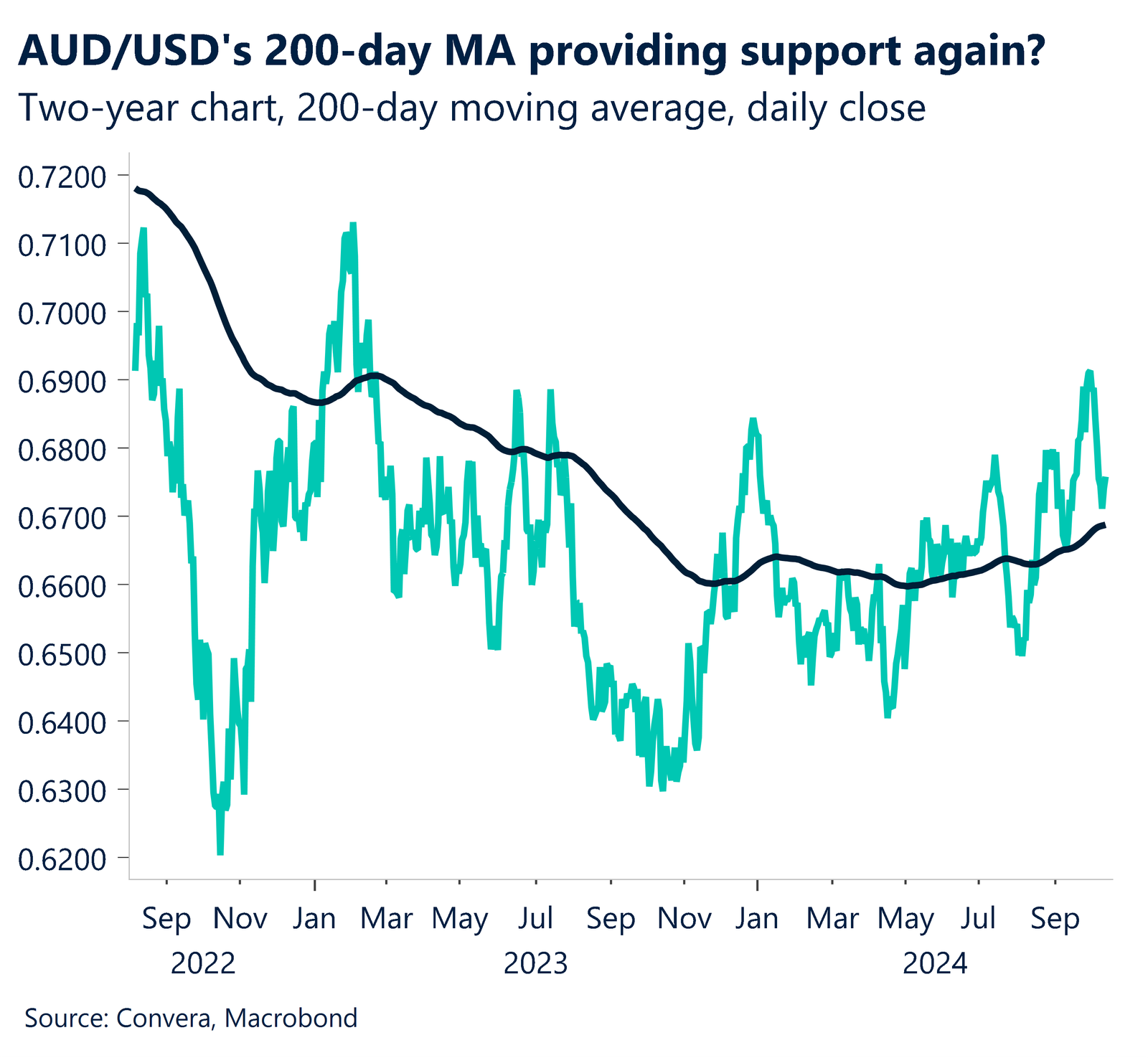

Asian FX markets have mostly started lower with the AUD/USD down 0.1% on Monday despite a better session on Friday helped by further gains in US sharemarkets.

On Friday, the Dow Jones gained 1.0% while the S&P500 climbed 0.6% — both reaching new all-time highs.

The NZD/USD was also lower on Monday with the kiwi still reeling from last week’s 50bps rate cut.

In Asia, the USD/CNH was higher in early trade as it continued the recent rebound from 18-month lows.

The USD/SGD was also higher ahead of today’s Monetary Authority of Singapore decision, seen as most likely to keep current policy settings in place.

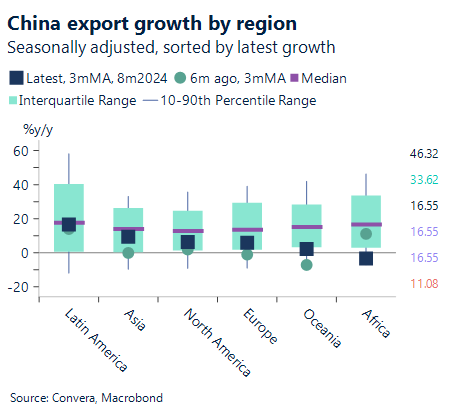

China trade balance to set tone for Asian markets

China will remain in focus with China’s imports and exports growth announced today.

August’s 8.7% year-over-year increase in exports is expected to drop to 5.6% in September as a result of a larger base and weaker external demand. Because of a smaller base, import growth is predicted to slightly accelerate to 2.1% y-o-y in September from 0.5% in August.

The government’s most recent stimulus package made it very evident that they are committed to fostering growth.

Even if the CNH has been stronger over the last three months, we believe that further strength is still possible in front of the US election, potentially weighing on USD/CNH.

Chart shows the breakdown of China exports by region.

MAS, ECB in focus as central banks meet

FX markets are set for a busy week ahead, with a mix of central bank decisions and major economic releases likely to drive currency movements.

The week kicks off with China’s trade balance report on Monday, setting the tone for Asian markets. As we move through the week, attention will shift to inflation data, with the UK and Canada releasing their CPI figures on Tuesday and Wednesday respectively.

Thursday will also see important data from the United States, with retail sales and industrial production figures providing insights into the health of the world’s largest economy. These releases could have significant implications for the US dollar and broader market sentiment.

Central banks will take centre stage this week, starting with Singapore’s Monetary Authority of Singapore decision on Monday. Bank of Thailand’s (BOT) monetary policy meeting is due on Wednesday.

However, the highlight for many traders will be Thursday’s European Central Bank (ECB) rate announcement. This decision is expected to be a key focus for market participants, potentially influencing the euro’s performance against major currencies.

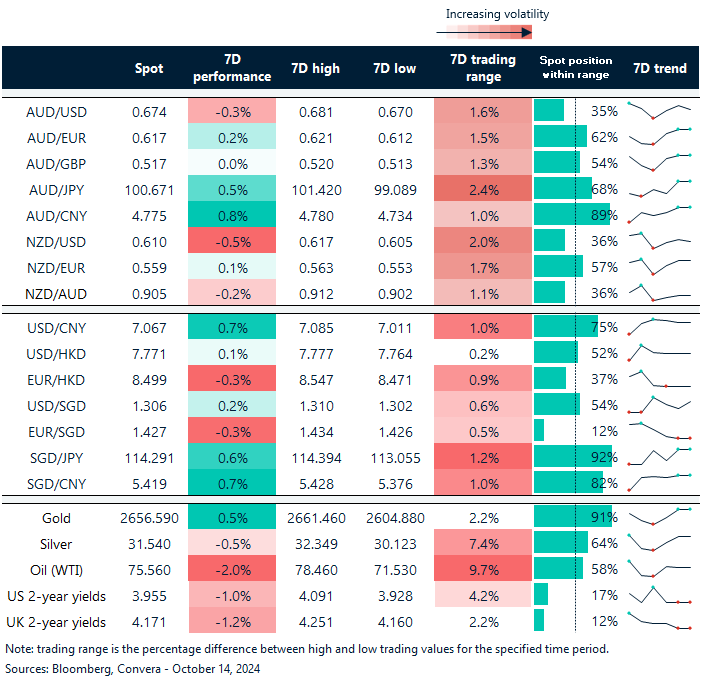

USD/SGD in focus ahead of MAS

Table: seven-day rolling currency trends and trading ranges

Key global risk events

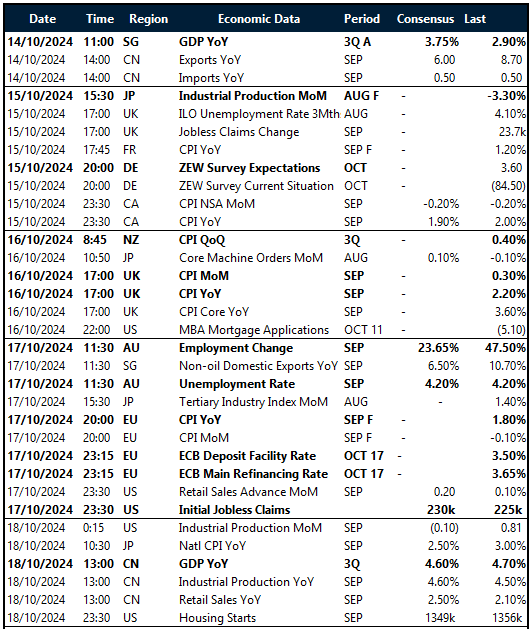

Calendar: 14 – 18 October

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}