Written by Convera’s Market Insights team

US yields slump despite inflation uptick

George Vessey – Lead FX Strategist

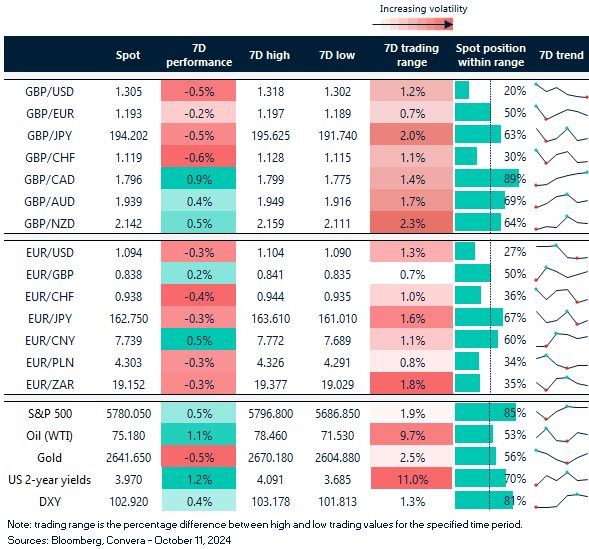

Market participants weighed up the slightly hotter-than-expected US inflation report versus the worse-than-expected jobless claims figure. The data means the battle between the labour market and inflation remains unsettled, but overall, money markets moved to increase bets on a quarter-point Fed rate cut in November. As a result, two-year US yields suffered their biggest daily drop of the month, though the US dollar index clocked its 9th daily rise in a row.

Elsewhere, US equity markets reached their 44th record high this week as the no-landing scenario has been gaining traction in the US. Economic momentum has turned north again, highlighted by the uptick of the surprise index into positive territory. Investors had reflected this narrative shift away from recessionary fears by pushing both the two- and ten-year Treasury yields beyond the 4% mark for the first time since early August, though the former dipped back below after yesterday’s initial jobless claims scare. The wall of worry continues to trouble investors across the world though. The 30-day implied volatility index (VIX) for the S&P 500 now incorporates the next US labour market report, presidential election and FOMC meeting and has risen well above its 2024 mean to 21.00. Markets have therefore started to incorporate the risks associated with the upcoming US election, which has raised hedging costs and FX volatility alike.

The race between Trump and Harris has essentially become too close to call and polls and betting markets remain within the margin of error. Price swings going into the election on November 5 will remain a feature of markets as the fluctuation of the implied winning probabilities lead to constant repricing in markets. A lean towards Trump in the betting polls could benefit the US dollar, while a rise of Harris on betting markets could elevate some pressure off EM FX.

Sterling shrugs off UK GDP rebound

George Vessey – Lead FX Strategist

The British economy expanded 0.2% m/m in August, after showing no growth in July, and in line with market expectations. The data has had little to no impact on the pound though. Having appreciated against 70% of its global peers last month, the pound has only appreciated against 16% of its peers so far in October. The main headwind has been the dovish repricing of Bank of England rate expectations, although UK yields have risen to their highest since July in the wake of higher US yields and arguably in anticipation of the UK Budget at the end of the month.

But the rise in oil prices and safe haven demand amidst the escalating conflict in the Middle East, has also constrained demand for risk-sensitive currencies, especially those of energy-importing nations, such as the UK. The euro is even is even more vulnerable though, hence sterling has only fallen 0.7% against the common currency month-to-date versus its 2.5% slide against the dollar. With the dollar’s safe haven appeal heading into a tight US election, GBP/USD downside risk is mounting and a break below $1.30 could be meaningful. A clean sweep for the Republican’s presents the biggest tail risk for the pound given its strong correlation with risk sentiment and the dollar’s expected positive short-term reaction to such a scenario.

Having broken below its 50-day moving average this week for the first time since August, the next target to the downside could be the 100-day moving average located at $1.2941 currently. However, if GBP/USD holds firm around this level, the bullish trend that’s been in place since October 2022, will remain intact.

French budget woes

Boris Kovacevic – Global Macro Strategist

The French equity benchmark has erased its year-to date gain as investors await changes to the government budget and an increase in taxes. Policy makers want to fill the €60 billion gap in the budget via 1) spending cuts, 2) temporary levies on some 440 companies with revenues of over €1 billion and other tax increases.

Asset managers have shunned French sovereign debt for a while now. Risk averse Japanese investors sold the debt of Eurozone’s second-largest economy for four consecutive months, signaling a turn away from France. The risk premium on holding French government bonds (vs. German ones) remains near its highest level since 2017. This fiscal dilemma explains the underperformance of the CAC 40 as earnings estimates have fallen so far this year, compared to a slight rise for the DAX and broader STOXX 600.

While not the most important factor driving euro weakness, French budget constraints have added downside pressures to the euro. The European Central Bank has recently shifted its tone to consider the next week’s October meeting a live one, at which markets are expecting a 25 basis point cut of the benchmark policy rates. At the same time, Fed rate cut bets have been pared back, leading to a rate differential moving against EUR/USD. The currency pair will likely end the week below the $1.10 mark after trading above it for seven consecutive weeks.

Dollar index holds in top 5% of 7-day range

Table: 7-day currency trends and trading ranges

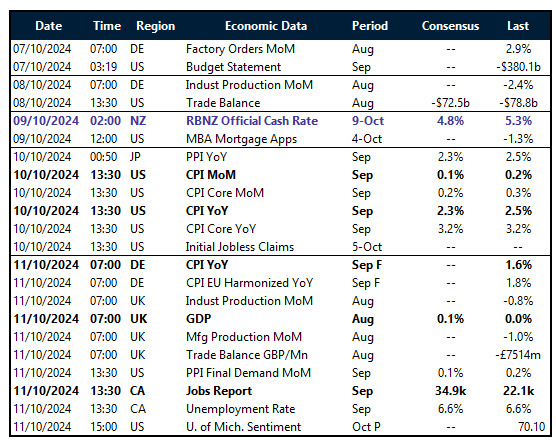

Key global risk events

Calendar: October 07-11

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}