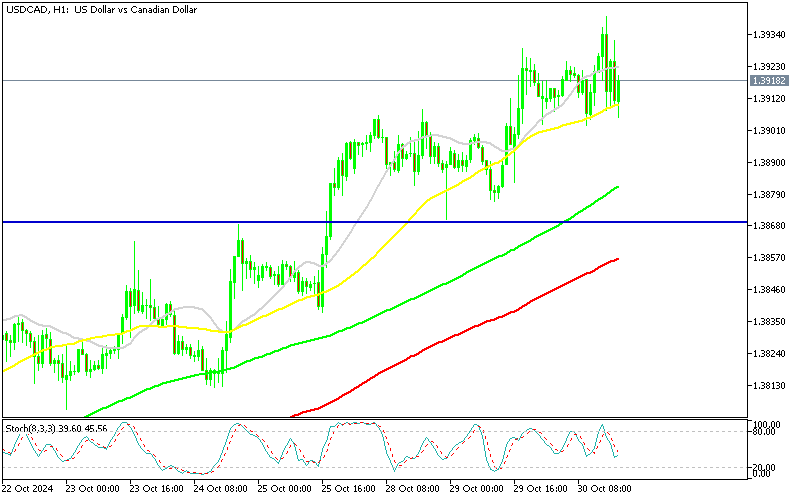

The economic data from the US today leaned on the positive side for the USD, but we saw a pullback on lower US GDP figures for Q3. The USD retreated but the pullback in USD/CAD seems weak, with MAS acting as support on the H1 chart, so we decided to open a buy forex signal here.

Employment growth exceeded expectations in October, with significant gains in services but a slowdown in goods-producing jobs. GDP growth in Q3 was slightly below expectations but still strong, driven largely by consumer spending and government expenditures. Core inflation indicators suggest easing, especially outside of core categories like food, energy, and housing, reflecting a lower inflation trend than previous quarters.

USD/CAD Chart H1 – MAs Continue to Hold As Support

The latest monthly PCE data points to a downward trend, with the headline PCE falling below the Federal Reserve’s 2.0% target. Core PCE has also moved closer to this objective, currently at 2.2%, down from 2.8%, which supports arguments for a possible policy recalibration. However, the strength of the recent jobs report somewhat complicates this view. Employment gains were widespread, led by sectors like education and health services, although manufacturing jobs saw a 19K decrease.

US ADP Employment for October

- Total Employment: +233K vs. +114K expected

- Previous Month: +143K

- Annual Pay Growth:

- Job-Stayers: +4.6% (vs. +4.7% prior)

- Job-Changers: +6.2% (vs. +6.6% prior)

- Sector Breakdown:

- Services: +211K (vs. +101K prior)

- Goods-Producing: +22K (vs. +42K prior)

ADP’s Chief Economist Nela Richardson commented, “Despite the hurricane recovery, job growth was strong in October. As we close out the year, hiring in the U.S. remains solid and broadly resilient.” This data underscores the labor market’s ongoing robustness, posing a potential challenge to arguments for easing monetary policy.

Q3 GDP (Advance Estimate)

- Growth Rate: +2.8% (vs. +3.0% expected)

- Previous (Q2 Final): 3.0%

- Contributions to Growth:

- Consumer Spending (PCE): +3.7% annual rate

- GDP Final Sales (excludes inventories): +3.0%

- Government Spending: +0.85% (vs. +0.52% prior)

- Net International Trade: -0.56% (vs. -0.90% prior)

- Inventories: -0.17% (vs. +1.05% prior)

- Business Investment: +3.3%

PCE and Inflation Metrics (Q3 Advanced):

- GDP Price Index (Deflator): +1.8%

- Core PCE:

- Q3: +2.2% (vs. +2.1% expected)

- Previous Quarter: +2.8%

- Overall PCE: +1.5% (vs. +2.5% prior)

- Ex Food, Energy, and Housing: +1.6% (vs. +2.3% prior)

- Services ex Energy and Housing: +2.6% (vs. 3.0% prior)

USD/CAD Live Chart

USD/CAD

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}